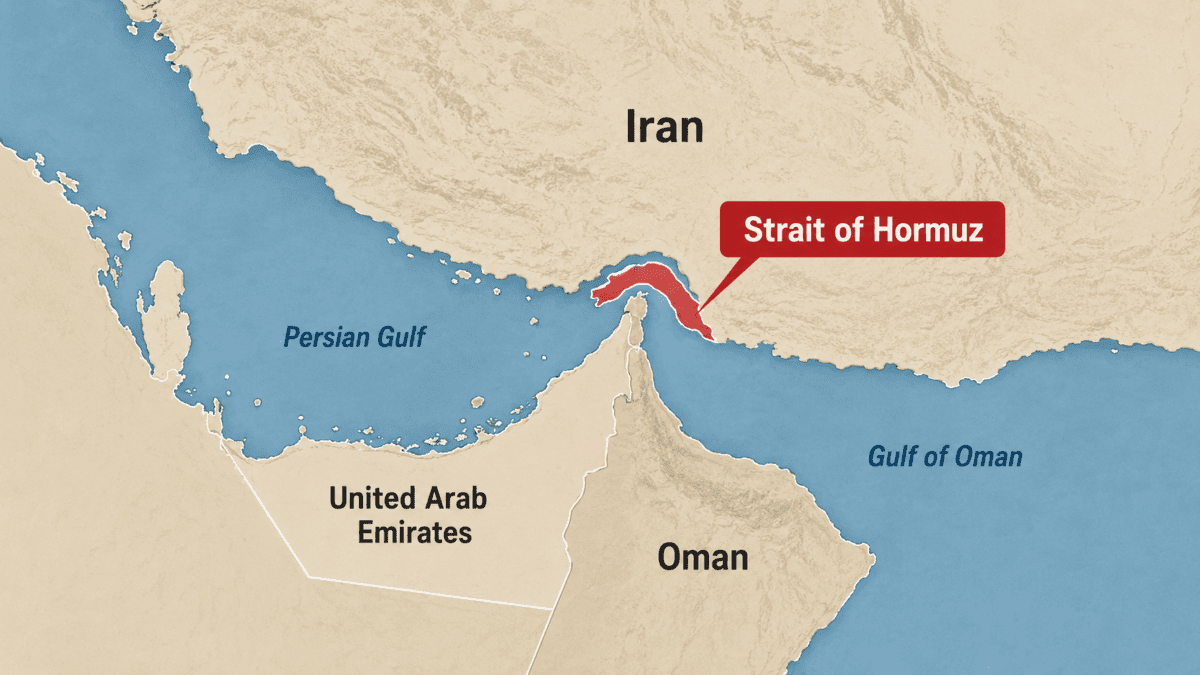

On February 28, the United States and Israel launched strikes against Iran. In retaliation, Iran’s Revolutionary Guard attacked merchant ships, laid sea mines, and blocked all passage through the Strait of Hormuz. Energy markets reacted within days. Brent crude crossed $120 per barrel. As a result, QatarEnergy declared force majeure on all exports. Meanwhile, Kuwait, Iraq, Saudi Arabia, and the UAE collectively lost at least 10 million barrels per day of output by mid-March. Consequently, the IEA called it the largest supply disruption in the history of the global oil market, comparing it to the 1970s energy crisis through its mix of supply shortages, currency volatility, and stagflation risk.

Despite early diplomatic pressure, the strait has not reopened. Trump threatened to obliterate Iranian power plants within 48 hours, then pulled back after describing talks as productive. In response, Iran’s defense council threatened to mine the entire Persian Gulf. In May, the UK deployed drones, fighter aircraft, and a Royal Navy warship to protect commercial shipping through the passage. Nevertheless, Iran’s IRGC now defines the strait as an Iranian operational area, and shipping risk premiums remain elevated.

While oil markets absorbed the first shock, fertilizer markets absorbed the second. Producers use natural gas as a primary feedstock for nitrogen-based fertilizers like urea and ammonia, so when gas prices rise, fertilizer production costs follow directly. Iran shut down ammonia production. Qatar suspended urea, ammonia, and sulfur output after strikes hit key facilities. Similarly, India cut urea and ammonia production as LNG supply tightened. As a result, the World Bank’s fertilizer price index climbed more than 12 percent in Q1 2026, its highest point since October 2022, with urea prices on track to rise nearly 60 percent across the full year.

Farmers carry this cost well before consumers notice it. The FAO warned that fertilizer scarcity will pull down yields and tighten food supplies through late 2026 and into 2027, because crop calendars do not wait. Specifically, fertilizers that miss the planting window cut yields permanently, regardless of what markets do afterward. Furthermore, suppliers are already routing fertilizer shipments toward wealthier buyers who can pay more, leaving import-dependent economies with what remains. As a consequence, higher energy, fertilizer, and transport costs now squeeze developing economies that already carry heavy debt and little fiscal room. The oil price, therefore, is not the full story. The real cost of the Hormuz closure will land in crop yields, food import bills, and household prices through 2027.